BTCW LN

WisdomTree Physical Bitcoin

Published 10 April 2026

Director, Digital Assets Research

Bitcoin’s price discovery has decisively migrated to derivatives markets. Futures, funding, and options positioning now set the marginal price; spot follows.

This is not a cyclical shift. It is structural. Ignoring derivatives today means systematically misreading bitcoin’s behaviour, particularly in periods of volatility, macro stress, or positioning extremes.

The dominant driver of bitcoin is no longer outright buying and selling. It is positioning expressed through leverage.

Bitcoin has evolved into a derivatives-led market, where perpetual futures drive price discovery, leverage cycles amplify moves via elevated open interest, and an increasingly relevant options complex introduces episodic dealer-driven flows around key strikes and expiries.

Price is no longer purely informational. It is mechanical.

The evolution of bitcoin derivatives is well understood, but the implication is often missed.

The key shift is not growth. It is dominance.

Derivatives are no longer an overlay. They are the primary venue of price formation.

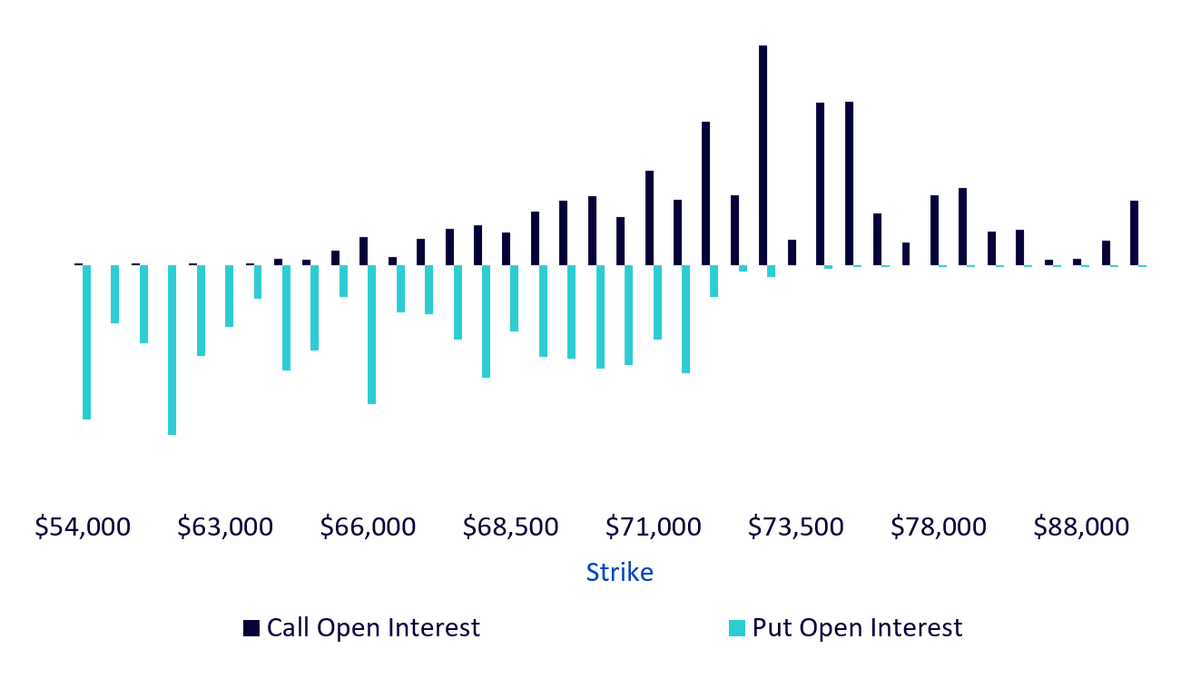

Option markets provide the clearest window into positioning, and increasingly, into future price behaviour.

The options strike map is effectively a distribution of risk:

Source: Bybit V5 Option Tickers. From 28 February 2026 to 07 April 2026. Historical performance is not an indication of future performance, and any investment may go down in value.

In the graph above, three zones matter:

At the same time, the spot bitcoin price sits at $71,519.

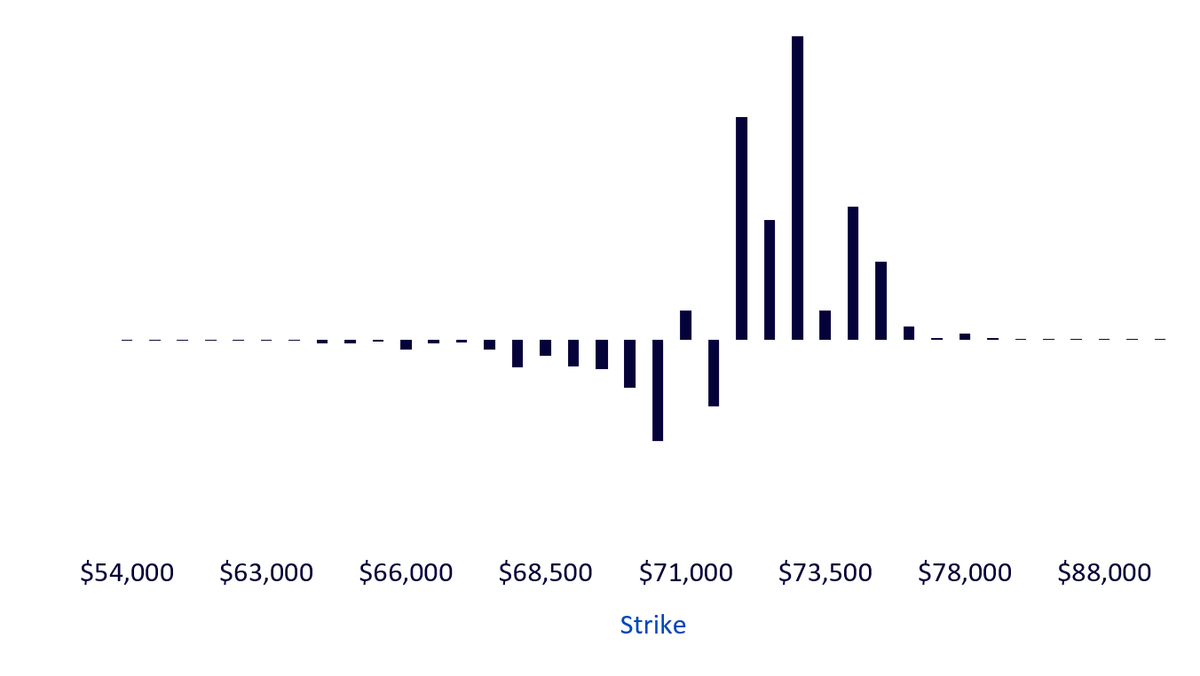

What matters is not just where positions sit, but how they translate into flows. That mechanism is dealer gamma:

The same positioning can therefore stabilise or destabilise the market depending on the underlying gamma profile.

Source: Bybit V5 Option Tickers. From 28 February 2026 to 07 April 2026. Net gamma (calculated as long gamma minus short gamma) is shown as a strike-level proxy inferred from public option open interest and implied volatility, not observed dealer inventory. Historical performance is not an indication of future performance, and any investment may go down in value.

This is where derivatives link directly into macro.

Liquidity conditions, exchange traded product (ETP) flows and rates do not impact bitcoin in isolation. They reshape leverage, positioning, and ultimately dealer hedging behaviour:

The result is a tightly coupled system where macro inputs flow through derivatives positioning into price. Bitcoin is no longer just reacting to fundamentals. It is reacting to how capital is positioned against them.

Short-term price is positioning-driven. Bitcoin moves are increasingly:

Volatility is structurally endogenous. Large moves no longer require new information as positioning alone can generate volatility. This is a fundamental shift from earlier market regimes.

“Technical levels” are now capital-backed. Levels like $59k-$61k or ~$73k are not abstract chart points:

Crowding risk is the dominant risk. When positioning becomes one-sided:

Monitoring funding rates, open interest, options skew is now core risk management, not optional analysis.

There is a counterpoint worth acknowledging:

But for any investors operating on tactical horizons or risk-managed portfolios, the distinction is academic. Path dependency is now the game.

WisdomTree Physical Bitcoin

Director, Digital Assets Research

Dovile Silenskyte is a director of digital assets research at WisdomTree. Before joining WisdomTree in May 2024, Dovile worked as an index equity product strategist at BlackRock. Currently, she is responsible for conducting analyses for in-house digital assets publications and assisting the sales team with client queries about products and markets. Dovile holds an MSc in Finance from Texas A&M University – Commerce, and she is also a chartered financial analyst (CFA).