The ‘hot picks’ leading the broad commodity rally

Published 13 March 2025

Luca Berlanda

Associate Director, Quantitative Research at WisdomTree in Europe

Key Takeaways

- Commodities are experiencing a widespread uptrend, supported by supply constraints, geopolitical risks, and strong demand.

- Natural gas is benefiting from cold weather and record LNG exports, aluminium from tariffs and supply cuts, coffee from weather-driven shortages and speculation, and gold from central bank demand and geopolitical uncertainty.

- Related Products WisdomTree Natural Gas, WisdomTree Coffee, WisdomTree Core Physical Gold Find out more

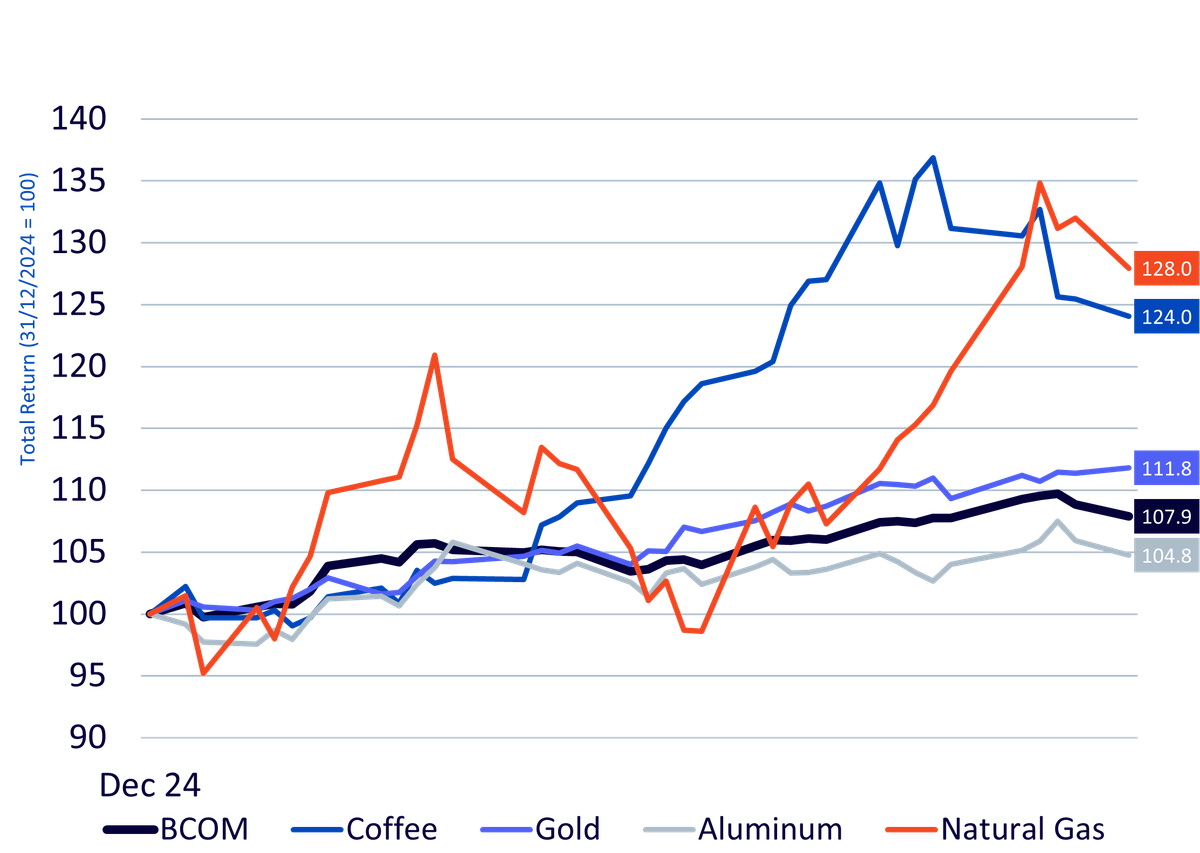

The broad commodities market has shown impressive strength in 2025, defying economic uncertainty and macroeconomic headwinds. Year-to-date (YTD), the Bloomberg Commodity Index (BCOM), widely regarded as the benchmark for broad commodity exposure, has risen by nearly 8% (see Figure 1). Several key commodities have surged, driven by supply constraints, geopolitical events, and shifting macroeconomic dynamics.

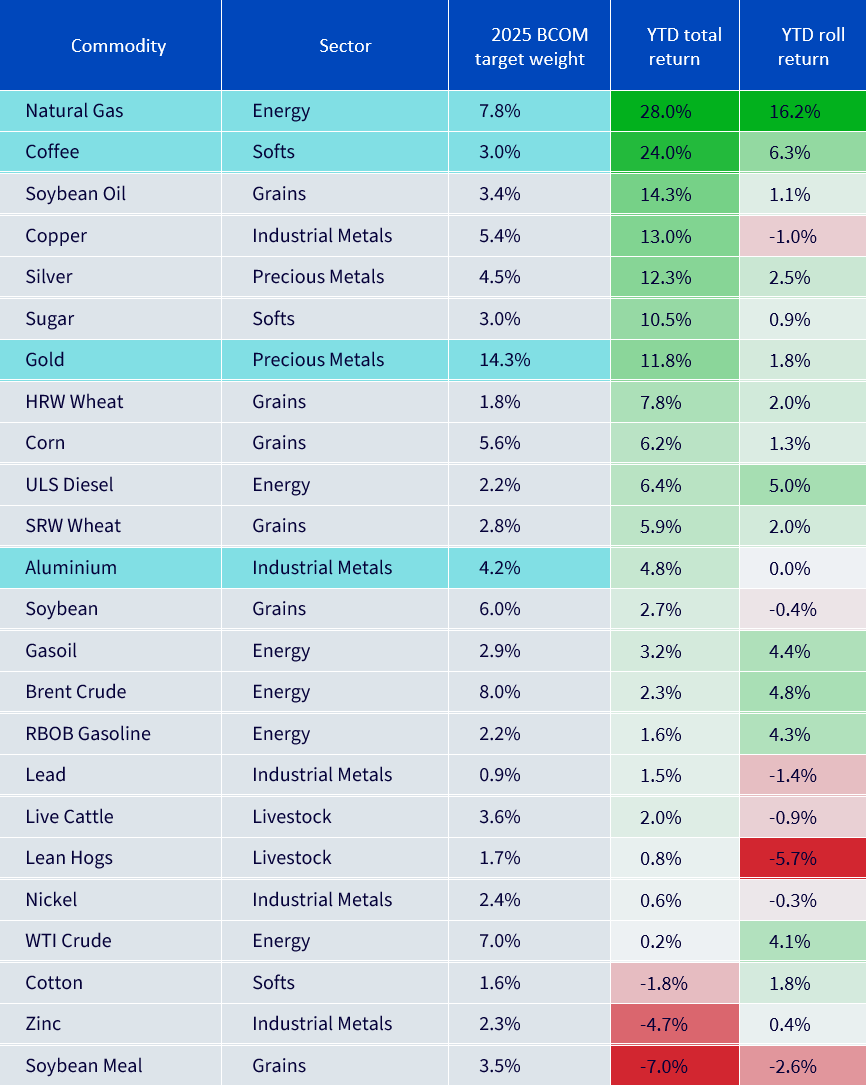

In Figure 2, we highlight the performance of all commodities within the BCOM index and their respective target weights for 2025. Notably, 21 out of the 24 commodities have posted positive YTD returns, indicating a broad-based rally rather than one dominated solely by a handful of heavyweight commodities.

In this blog, we spotlight four standout commodities—natural gas, aluminium, coffee, and gold—each representing a major sector within the broader commodity space. We will explore the factors driving their bullish trajectory and what may lie ahead.

Natural gas (sector: energy)

US natural gas has experienced significant price gains this year (+28% on a total return basis1), driven by a confluence of weather-related demand spikes and structural shifts in global supply. The extreme cold snap that gripped the US early in the year led to a sharp rise in heating demand, pushing Henry Hub Natural Gas prices higher. As temperatures dropped below seasonal norms, storage withdrawals exceeded expectations, tightening available supply and driving prices up.

Adding to this bullish momentum, US Liquefied Natural Gas (LNG) exports have hit record highs. Europe’s continued efforts to secure alternative energy sources—away from Russian gas—have resulted in sustained demand for US LNG. At the same time, production cuts in the US due to weather-related disruptions further exacerbated the supply-demand imbalance. Looking ahead, the interplay between storage levels, weather patterns, and global LNG demand will dictate price action. With expectations of continued colder-than-normal temperatures and geopolitical tensions still affecting energy markets, natural gas remains a volatile but potentially promising bet.

It's also worth noting that of the total 28% return, 18.4% can be attributed to roll yield2. This is particularly significant given that the natural gas forward curve has shifted into backwardation in recent months. This shift has allowed investors to benefit from positive roll returns, a rarity in a market where the cost of carry is usually high. However, it's important to note that natural gas is heading back into seasonal contango and that, to maintain strong performance, spot prices will need to move significantly higher to offset the negative roll returns.

Aluminium (sector: industrial metals)

Aluminium has emerged as a strong performer in the industrial metals complex, with prices rising above $2,700 per metric ton3, marking a nine-month high. A key driver has been the US government’s announcement of increased tariffs on aluminium imports, particularly affecting supply chains from major exporters such as Canada.

On the global stage, production cuts in China have also played a crucial role. With Beijing enforcing strict production caps and carbon emission targets, aluminium smelters have been forced to slow down operations, tightening global supply.

Meanwhile, demand remains robust, particularly from sectors benefiting from the energy transition. Aluminium is a critical material in electric vehicles, renewable energy infrastructure (such as solar panels and wind turbines), and power transmission lines. This structural demand, combined with supply constraints, sets the stage for sustained strength in aluminium prices.

Additionally, an unusual front-month backwardation has formed in the aluminium futures curve; while the YTD roll yield has been mildly negative, the recent shift into backwardation underscores increasing supply tightness.

Coffee (sector: agriculture and livestock)

Arabica coffee prices have skyrocketed, recently surpassing $4.30 per pound—a level not seen in years. This surge can be attributed to a combination of supply-side disruptions and speculative market positioning.

Brazil, the world’s largest Arabica coffee producer, has been hit by prolonged drought conditions since April 2024. With crops under stress, yield expectations for the upcoming harvest have been revised downward. The biennial bearing cycle of Arabica coffee, which alternates between high and low production years, is exacerbating the tight supply outlook. 2024/2025 season was supposed to be a high-yield season, but adverse weather has limited the output gains.

On the speculative front, the Intercontinental Exchange (ICE) recently increased margin requirements for Arabica coffee contracts, forcing short traders to unwind positions. This liquidation of shorts fueled further upside momentum, creating a self-reinforcing price rally. Looking ahead, weather patterns in Brazil, the evolution of speculative positioning, and global supply chain disruptions will determine the future trajectory of coffee prices.

Gold (sector: precious metals)

Gold has, once again, proven its resilience, climbing steadily despite a strong US dollar and rising bond yields—two factors that typically weigh on the precious metal. The key bullish forces driving gold’s performance in 2025 include heightened geopolitical risks, central bank demand, and inflation concerns.

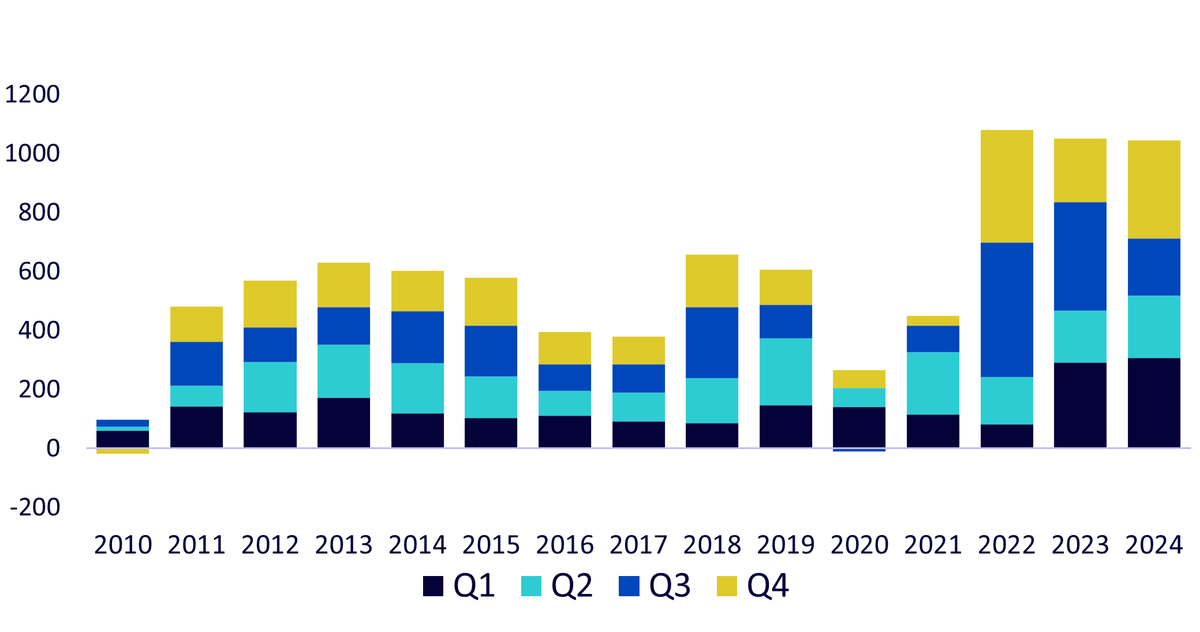

One of the most significant structural drivers has been robust central bank buying. According to the World Gold Council, central banks have continued their gold accumulation, with purchases remaining near record levels (2024 central banks’ gold purchases have been just 1% lower than 2023, with a very strong 4th quarter in 20244). This trend has been particularly strong among emerging market economies looking to diversify reserves away from the US dollar.

Meanwhile, gold’s safe-haven appeal has been reinforced by geopolitical instability. Ongoing conflicts and trade tensions have driven investors toward gold as a hedge against uncertainty. Furthermore, inflationary pressures remain a concern, with global central banks walking a fine line between controlling price increases and maintaining economic stability. If inflation expectations rise further, gold could see additional upside momentum.

Conclusion

The broad commodities complex has had a strong start to 2025, with natural gas, aluminium, coffee, and gold leading the charge. Structural supply constraints, geopolitical tensions, speculative positioning, and strong demand fundamentals have all contributed to the recent gains. While volatility remains a factor, these commodities continue to present compelling investment opportunities.

1Bloomberg, WisdomTree. Data from 31-12-2024 to 24-02-2025.

2Ibid.

3Ibid.

4WisdomTree, World Gold Council, Q1 2010 to Q4 2024.

Categories

Related articles

About the contributor

Luca Berlanda

Associate Director, Quantitative Research at WisdomTree in Europe

Luca is an Associate Director in WisdomTree Europe's Research team, where he conducts quantitative research to enhance or develop new investment strategies, particularly in commodities and thematic equities. He also focuses on portfolio construction and optimisation. Before joining WisdomTree in 2022, Luca worked as a Quantitative Portfolio Manager at Euclidea SIM, a Milan-based fintech where he quantitatively managed multi-asset portfolios and developed and implemented statistical and machine learning models for investment strategies and fund selection. Luca holds a Master's degree in Finance from Bocconi University, Milan.