COCO LN

WisdomTree Cocoa

Published 5 April 2024

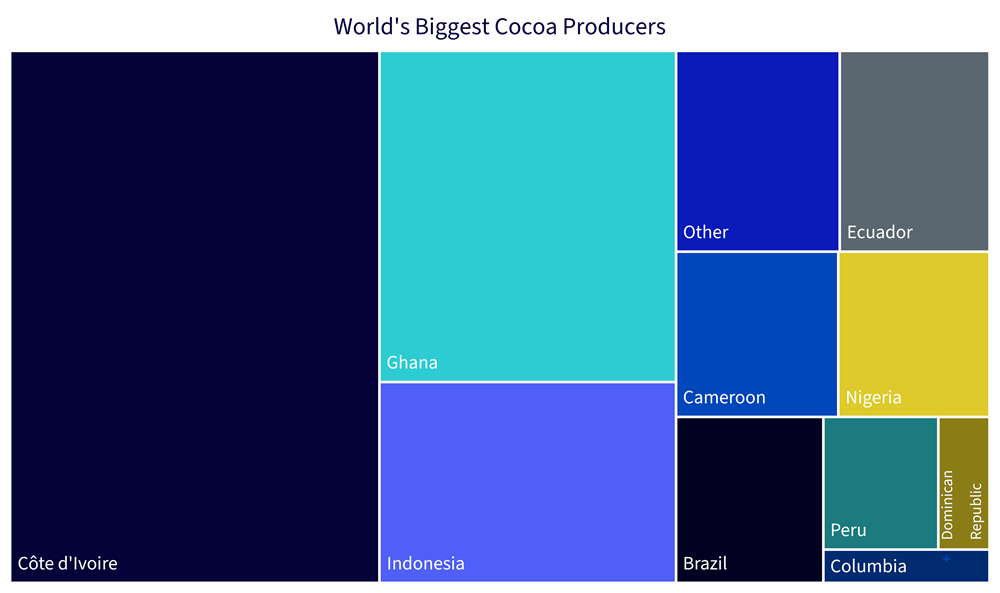

Cocoa’s meteoric price rise +132% has trumped both Nvidia (+90%) and Bitcoin’s (+65%) price performance in Q1 20241. The cocoa market has been struggling with poor crops in major producing regions in West Africa. Two west African countries, Côte d’Ivoire (Ivory Coast) and Ghana represent about 60% of the world’s cocoa production. Dry weather brought by the El Niño followed by unseasonal heavy rains towards the end of 2023, escalated concerns about West African production as discussed here. Additional factors such as extreme heat, ageing cocoa trees and illegal mining have further exacerbated supply shortages.

Source: United Nations (UN) Food and Agriculture Organization (FAO) as of December 2023

News reports and trade publications indicate cocoa bean processing in West Africa is finally being shut-in and running at low utilization throughout March owing to the lack of supply. Cocoa grindings – a good proxy for demand is expected to decline given the fall in supply. We expect to see demand destruction at the user level start to garner momentum over Q2 2024. However, as processing demand only started to meaningfully decline in March 2024 and has held up moderately in both Europe and North America, we do not see increased risk of consumption rolling over.

Ghana will raise the fixed farmgate price paid to cocoa farmers by up to 50% in an effort to share profits from rising global prices and deter farmers from bean smuggling2. Low pay has hampered farmers’ ability to invest in improvements and fend off disease, limiting the yield of cocoa trees. According to Cocobod, 150 thousand tons of cocoa beans were lost in the 2022/23 crop year due to this and illegal gold mining. This crop year (2023/2024), the loss is likely to be larger owing to higher prices. Ivory Coast has already increased farm-gate prices for cocoa farmers by 50% to the equivalent of US$2470 per ton3.

In the short term, its unlikely to stall cocoa’s price rally as it takes around 5 years for a newly planted cocoa tree to develop pods for the first time. However, over the long term, higher farm-gate prices could incentivise farmers in Ivory coast and Ghana to invest more in the maintenance of their cocoa plantations thereby supporting a price dampening effect.

Cocoa is harvested twice a year. The main crop runs from October to March, while the mid-crop runs from April to August. Investors’ attention is likely to turn towards the upcoming mid-crop harvest in West Africa.

The crop in Cote d’Ivoire, by far the most important producer with a market share of around 40% is expected to be only 400-500 thousand tons, versus 600 thousand tons reported last year. These estimates are based on a survey carried out by the national regulator at the end of February. Normally the mid-crop holds less importance in comparison to main crop owing to its smaller size (in the case of Cote d’Ivoire, around 25% of the total crop). However given the already weak main crop, it is likely to dominate investor attention this time around. If estimates are downgraded further, it could provide another catalyst to cocoa’s current price rally.

The International Cocoa Organisation (ICCO) also projected the ratio of stockpiles to grindings will fall to the lowest in more than four decades this season. ICCO also expects the existing supply deficit to widen to 374kt this season, versus a deficit of 75kt seen last season.

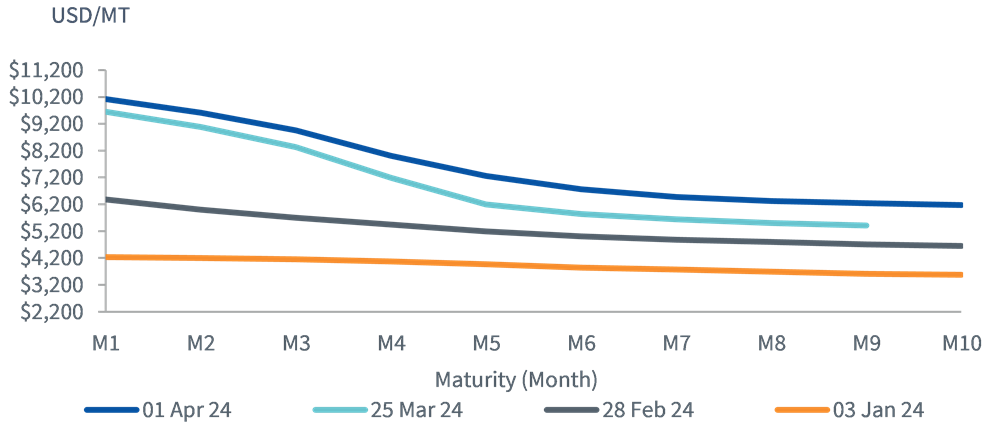

The front end of the cocoa futures curve remains in backwardation, giving rise to a 5.3% positive roll yields (versus 6.4% last month). The weather is likely to play a crucial role in shaping the market balance for the season.

Source Bloomberg, WisdomTree as of 2 April 2024. Historical performance is not an indication of future performance and any investments may go down in value.

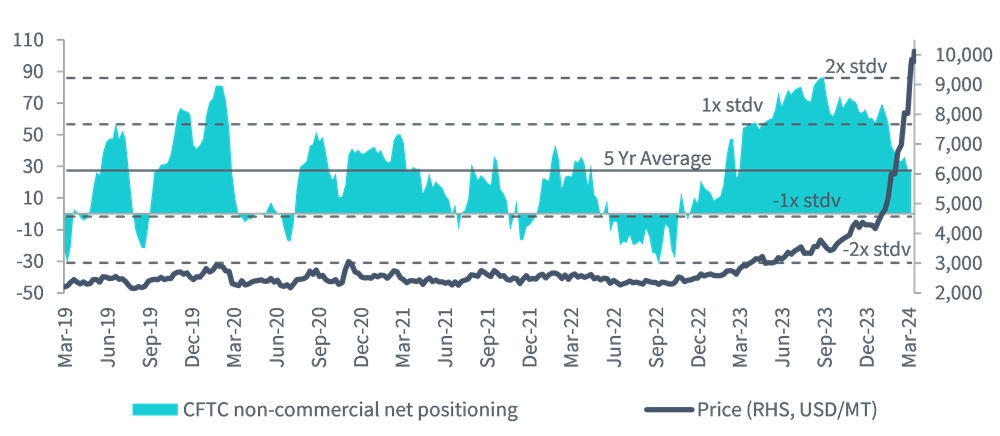

Net speculative positioning has declined 21.9% over the prior month (from 27 February 2024 to 26 March 2024) according to Commodity Futures Trading Commission (CFTC). CFTC data shows that investors remain undecided on extension of cocoa’s rally evident from the 27% decline in short positioning alongside a 24% reduction in long positioning.

Source: Commodity Futures Trading Commission (CFTC), WisdomTree as of 1 April 2024. Historical performance is not an indication of future performance and any investments may go down in value.

1 Source: Bloomberg from 2 January 2024 to 28 March 2024

2 State Marketing Authority Cocobod

3 The Business Times as of 31 March 2024

WisdomTree Cocoa

Director, Macroeconomic Research, WisdomTree Europe

@AneekaGuptaWTAneeka Gupta is Director of Research at WisdomTree. Prior to the acquisition of ETF Securities in April 2018, Aneeka worked as an Equity & Commodities Strategist at the company. Aneeka has 17 years of experience working as a Research Analyst across a wide range of asset classes. In her current role she is responsible for conducting analysis for all in-house equity, commodity and macro publications and assisting the sales team with client queries around products and markets. Prior to WisdomTree, Aneeka began her career as an equity analyst at Bear Stearns International Ltd in London. She also worked as an Equity Sales Trader at Sunrise Brokers across US and Pan European Exchanges. Before that she worked as an Equity Derivatives Sales Manager at Mashreq Bank in Dubai. Aneeka holds a Masters in Mathematics from Oxford University and a BSc in Mathematics from the University of Delhi, India. She is also a CFA Charterholder.