How to use ETPs to hedge fixed income portfolios

Published 4 August 2017

Contributor

Fixed income has been at the heart of European investor portfolios for many years with average allocations in 2016 standing at 51%. Even in an environment of low or negative yielding domestic government bonds, overall allocations have remained high. Now Eurozone government bond investors are overwhelmingly focused on the risks relating to the end of quantitative easing and the potential for a rise in interest rates at some point in 2018.

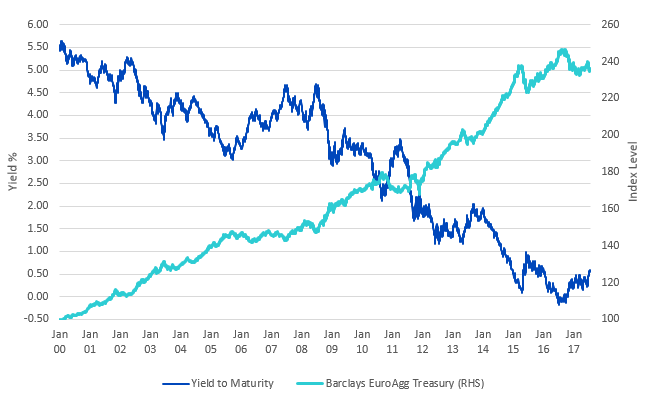

Markets have already had a sharp correction from the unparalleled instances of 10-year Bund yields hitting a low of -0.2% in early July 2016. Since its peak in early August 2016, the Bloomberg Barclays Euro Aggregate Treasury Index has fallen by over 4.1%. This contrasts with overall annualised returns of over 4.8% that investors have enjoyed from 1998 to the end of 2016.

Chart 1: Euro government bonds at close to all-time highs

Source: Bloomberg, WisdomTree

Hedging fixed income portfolios amidst a turbulent environment

The challenge now is how to hedge broad Eurozone fixed income portfolios against the possibilities of a more turbulent market environment. One of the main constraints for investors is often an inability to hedge using instruments such as futures, swaps or options. These can be complex to manage with respect to margin, total risk and exposure management. In this context, ETPs may be used to provide an operationally efficient and cost-effective hedge. As ETPs are listed and traded on exchange, investors may benefit from multiple liquidity providers, full transparency of pricing, TER and swap costs. Investors still need to be conversant with the technical aspects of short and leveraged ETPs such as daily rebalancing, compounding and the over-collateralised swap structure.

To illustrate the benefits of hedging using ETPs we have considered the period covered from when Bund yields moved into negative territory and then normalised, and is relevant to an environment where rising rates are likely to feature.

Using ETPs in practice

At a portfolio level, using a 3x Short ETP means that an investor only needs to commit 25% of the total portfolio value into the ETP to create a fully hedged position. This is due to the capital efficiency inherent in the -3x leveraged ETP, comparing favourably with other short ETPs that offer either -1x or -2x exposure. When initiated, the portfolio is 100% hedged and by its very nature this hedge ratio is likely to evolve based on the performance of both the portfolio and the hedging instrument. To maintain an efficient hedge that can provide an appropriate level of portfolio protection it is usual to maintain the hedge ratio within certain conservative boundaries. In our example, we have chosen +/- 5% as the threshold away from being 100% hedged as it may be beneficial to rebalance the hedge ratio back in line to 100%.

Chart 2: The performance of the hedged and unhedged portfolio

Click to enlarge

Source: WisdomTree, Bloomberg

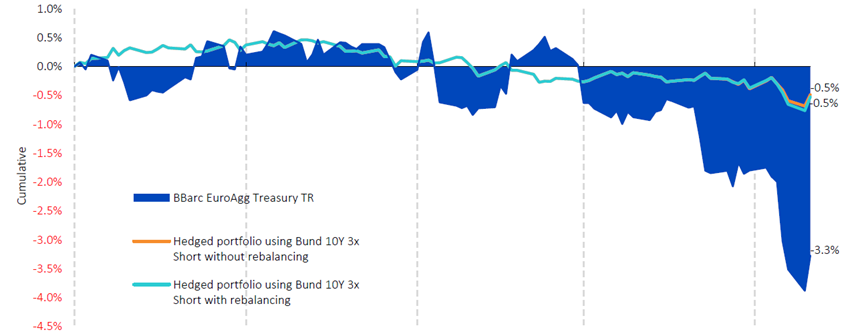

In the context of a fixed income portfolio, with volatility as low as 4.3%, it is also possible that there may be relatively little need to rebalance. In our example, there are two rebalances over the four-month hedging period and the resulting hedged portfolio has annualised volatility of 1.3% and overall returns -0.5% compared to an unhedged portfolio that would have returned -3.3%. In terms of other risk measures, an unhedged portfolio over the same period would have experienced a maximum drawdown of 4.5% whilst the hedged portfolio was constrained to 1.2%.

Chart 3: The impact of rebalancing

Click to enlarge

Source: WisdomTree, Bloomberg

The costs associated with hedging

Apart from the fact that the hedge performed efficiently, it is also important to note the overall transaction costs for putting on, rebalancing and unwinding the hedge. As the Bund Rolling Future Index consists of front-month Euro-Bund futures, the spreads and transaction costs reflect those of the underlying. Based on historic data the total transaction costs for the hedge are estimated at less than 5bps.

Short fixed income ETPs may represent an operationally and capital efficient means of protecting broad fixed income portfolios from upcoming macro and interest rate risks. Compared to other short ETPs with lower leverage, -3x or -5x can significantly lower total portfolio volatility. After a prolonged multi-year bull market in fixed income and with considerable risks ahead with the unwinding of quantitative easing by the ECB and the possibility of a gradual albeit modest rise in interest rates in 2018, investors may wish to contemplate hedging their fixed income exposures.

You may also be interested in reading…

Categories

About the contributor