Europe’s “back to normal” leaves safe havens at risk: Should you hedge German Bunds?

Published 27 September 2017

Contributor

The European political uncertainty and risks posed to financial markets are—for now—over. A Liberals-led mainstream coalition in The Netherlands firmly aligned with Germany’s EU agenda and a pro-European President of France upending fringe/extreme sentiment preserves the status quo. Also, Germany’s election in September was largely a non-event with Merkel this year leading early on in the polls and the Social Democrats headed by Martin Schulz as runner up. The far right AFD coming as third largest was the main surprise and will complicate Merkel’s efforts to create and run a coalition government. Italy is unlikely to have its election until 2018.

But there remains plenty of downside risks for Europe’s bond markets, more notably a widely anticipated 4th and 5th rate hike by the Fed since 2015 and more “upbeat” statements from the ECB on the Eurozone’s economic outlook to instigate renewed speculation of an early QE taper.

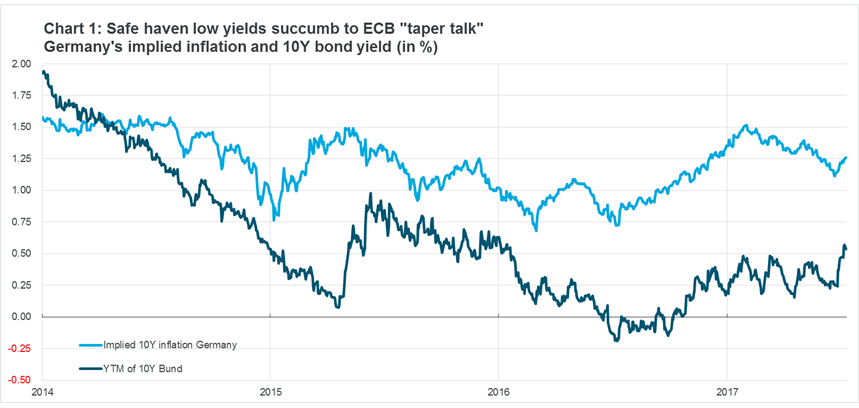

Most prone to volatility and downside risk are German Bunds that trade on bedrock yields.

Aside from the risks of the Fed and ECB tightening, there is talk of French President Emmanuel Macron looking to introduce “eurobonds” in his legislative agenda, that by implication would mean more burden sharing by the EU’s prime creditor members to finance weaker EU members’ investments needs—something that is not going to help sentiment in German Bunds. Furthermore, robust jobs and wage growth underpin a sustained higher German inflation outlook, even as the outlook for China and trade stabilises and OPEC orchestrates further curbs to oil production.

With the veil of political uncertainty in Europe removed for now, German Bunds stand newly exposed to robust raw economic fundamentals to make the already crowded trade increasingly hard to justify. The erratic 20 to 50 bps yield around which German Bunds have been trading since the start of the year suggest investor confidence in Bunds’ resilience is weak, not least if 180-200 bps more value (yield) can be extracted from long dated US Treasuries. And with inflation at 2%, Germany’s institutional investors will find it difficult to continue to justify matching domestic long-term liabilities against yields that against both implied (that is, forward-looking) and actual inflation given inflation-adjusted are now so deep in negative territory.

Source: WisdomTree, Bloomberg

Hedging Bunds using leveraged inverse ETPs

Investors looking to protect their European government bonds may consider using leveraged short ETPs as hedging instruments. For short and longer-term investment horizons, leveraged short ETPs tracking high grade fixed income could be efficiently deployed.

Leveraged short ETPs control leverage through the daily rebalancing mechanism and as a fully pre-funded arrangement, limit the maximum loss to the initial capital outlay. This is unlike derivative instruments that trade on margin where losses can exceed the original investment.

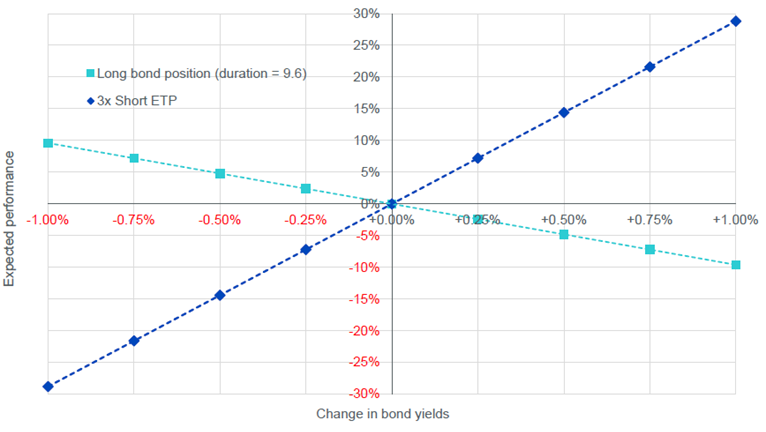

Investors should be mindful of the high sensitivity long-dated bonds have on relatively small changes in interest rates, as is shown in Chart 2 below. Using the concept of duration allows one to approximate a bond’s price sensitivity to changes in yield. This suggests that a hypothetical high grade long-dated bond investment, such as 10Y German Bunds, which currently have a duration of 9.6, would decline by 2.4% based on a 25bps rise in bond yields (0.25% x 9.6)1. A 50bps rise in bond yields would decrease bond prices by approximately 4.8%.

The current macro backdrop of low yields and higher inflation have subjected German Bunds to erratic fluctuations in yields this year. Investors could think of such volatility and losses as realistic for high grade European government bonds, and as understated for lower grade sovereigns such as Italian BTPs, where downside risk is perceived to be greater.

Chart 2 shows how, in this simplified concept of duration, interest rate risk is hedged using a 3x short ETP—the leveraged inverse exposure to the hypothetical 10Y bond investment. As shown by the blue line, a 25bps rate rise scenario would raise the price of 3x short ETPs by 7.2% (0.25% x 9.6 x -3, see Chart 2), three times the inverse return of the underlying (3 x -2.4%).

Chart 2: Hedging a hypothetical bond using leveraged inverse ETPs

Sensitivity of leveraged short ETPs and the underlying to interest rate changes

Source: WisdomTree, Bloomberg

To fully hedge your long position using a 3x short ETP for one day, the initial capital required is 33.3% of the long position. Assuming a US$1m investment in 10Y government bonds with duration of 9.6 the impact of rising yield to the bond portfolio with a 9.6 duration may be the following:

Long position The market value falls by: | Short position The notional value rises by: | Net gain/loss | |

|---|---|---|---|

Bond yields rise by 25 bps | US$24k ($1m x -0.25% x 9.6) | US$24k (US$333k x -0.25% x -3 x 9.6) | $0 |

Bond yields rise by 50 bps | US$48k (US$1m x -0.50% x 9.6) | US$48k (US$333k x -0.50% x -3 x 9.6) | $0 |

Long position

The market value falls by:

Short position

The notional value rises by:

Net gain/loss

Bond yields rise by 25 bps

US$24k ($1m x -0.25% x 9.6)

US$24k (US$333k x -0.25% x -3 x 9.6)

Bond yields rise by 50 bps

US$48k (US$1m x -0.50% x 9.6)

US$48k (US$333k x -0.50% x -3 x 9.6)

Investors looking to limit downside risk could consider partially hedging their long exposure. Assuming a 50% hedge, the capital committed for the short position using a 3x short ETP is 16.7% (0.5 x 33.3%) of the long position. For a US$1m investment in 10Y government bonds, the impact of a 25 and 50 bps rate rise to the portfolio could be the following:

Long position The market value falls by: | Short position The notional value rises by: | Net gain/loss | |

|---|---|---|---|

Rates rise by 25 bps | $24K ($1M x -0.25% x 9.6) | $12K ($166.7K x -0.25% x -3 x 9.6) | $-12K |

Rates rise by 50 bps | $48K ($1M x -0.50% x 9.6) | $24K ($166.7K x -0.50% x -3 x 9.6) | $-24K |

Long position

The market value falls by:

Short position

The notional value rises by:

Net gain/loss

Rates rise by 25 bps

$24K ($1M x -0.25% x 9.6)

$12K ($166.7K x -0.25% x -3 x 9.6)

Rates rise by 50 bps

$48K ($1M x -0.50% x 9.6)

$24K ($166.7K x -0.50% x -3 x 9.6)

High-grade limits the effect of compounding

What about the effect of compounding on holding periods that extend over several weeks or months?

Because short ETP returns are leveraged (in our example by 3x), the effect of daily compounding over longer holding periods is magnified. The more volatile the underlying, the greater the risk is that the actual performance of the leveraged short ETP deviates from the expected performance (that is, the cumulative performance of the underlying multiplied by the leverage factor). However, in the case of high grade government bonds such as German Bunds, the drift tends to be small. Underpinned by low volatility of around 4%, holding periods of several weeks in 3x short ETPs tracking German Bunds have realised returns that closely match expectations.

This is also shown in Chart 3 where holding 3x short ETPs tracking 10Y German Bunds over any 20-day period since the EU referendum, a time of heightened political uncertainty in Europe, would have produced inverse returns close to 3x the underlying.

Chart 3: Sensitivity of leveraged short ETPs and the underlying to interest rate changes

Source: WisdomTree, Bloomberg. Data form 23 June 2016 to 16 May 2017. * Used here is Boost Bund 10Y 3x Short Daily ETP (3BUS). ** Used here is the underlying index of German Bund futures 3BUS tracks.

Conclusion

Investors should not underestimate the riskiness of the environment for German Bunds, with a mixture of inflationary expectations and the end of QE posing challenges for the fixed income market. Short ETPs can provide an efficient means to hedge positions in high-grade government debt such as German Bunds, US Treasuries or UK Gilts, even over longer holding periods. It also means that little rebalancing is required to maintain the targeted hedged position, making short ETPs cost-effective instruments for hedging bond portfolios.

Our offering

+ Boost BTP 10Y 3X Leverage Daily ETP (3BTL)

+ Boost Bund 10Y 3x Leverage Daily ETP (3BTS)

+ Boost Bund 10Y 3x Short Daily ETP (3BUL)

+ Boost Gilts 10Y 3x Leverage Daily ETP (3GIL)

+ Boost Gilts 10Y 3x Short Daily ETP (3GIS)

+ Boost US Treasuries 10Y 3x Leverage Daily ETP (3TYL)

+ Boost US Treasuries 10Y 3x Short Daily ETP (3TYS)

+ Boost BTP 10Y 5X Short Daily ETP (5BTS)

About the contributor