What's Hot: Fed independence in the balance and implications for the dollar

Published 1 September 2025

Key Takeaways

- Markets are pricing in a potential September rate cut after Powell's Jackson Hole remarks, pressuring the dollar

- Political risks, including challenges to Fed independence, are introducing a governance-driven risk premium that could destabilize the dollar’s safe-haven appeal

- Investors can respond to dollar fragility with diversified strategies across gold, Treasuries, and tactical currency exposures—while bitcoin emerges as a hedge against institutional erosion

- Related Products WisdomTree Physical Gold - EUR Daily Hedged, WisdomTree Physical Gold - GBP Daily Hedged, WisdomTree Short USD Long EUR, WisdomTree US Treasuries 30Y 3x Daily Short, WisdomTree Physical Bitcoin Find out more

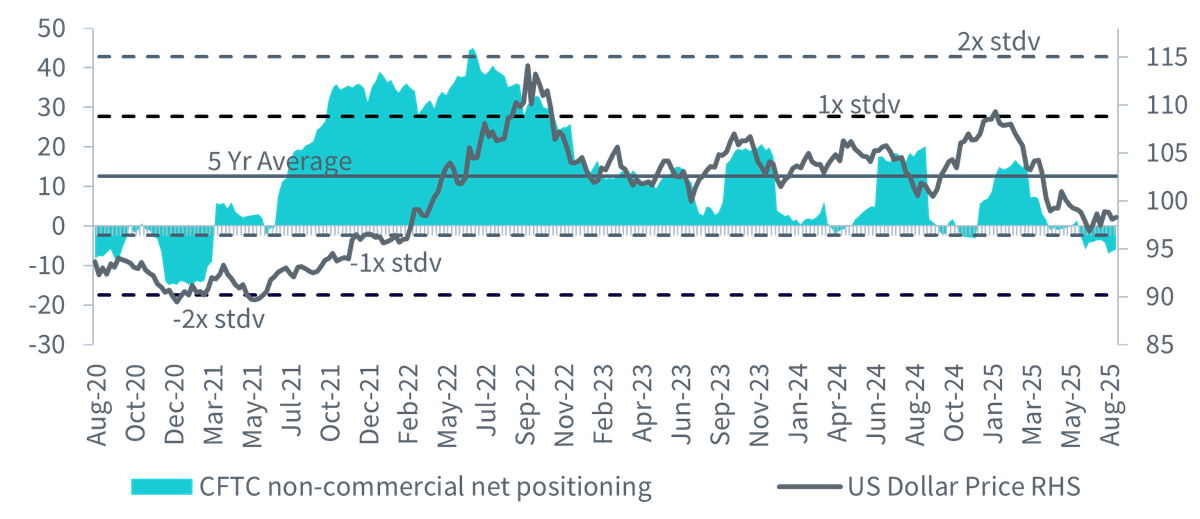

Markets entered late summer focused squarely on policy rather than politics. At Jackson Hole in August, Federal Reserve (Fed) Chair Jerome Powell signalled that a rate cut as soon as September is on the table, citing rising risks to the labour market while keeping a close watch on inflation. Futures quickly priced a high probability of a 25 Bps rate cut. Data from the Commodity Futures Trading Commission (CFTC) confirms that sentiment towards the US dollar remains weak. Net speculative positioning on the US Dollar is more than 1-standard deviation below the 5-year mean.

Figure 1: Net speculative positioning on the US dollar

Source: Commodity Futures Trading Commission (CFTC), WisdomTree as of 19 August 2025. Historical performance is not an indication of future performance and any investments may go down in value.

For the dollar the immediate impulse from easier policy is negative, though any weakness can be tempered if the Fed convinces investors that the easing cycle will be gradual and still anchored in a 2% inflation objective.

Governance risk through a market lens

The potential removal of Fed Governor Lisa Cook is an institutional development that deserves a place in the macro conversation. The White House has cited mortgage related allegations as sufficient cause, while Governor Cook has denied the claims and argues that the president lacks authority to remove a governor midterm. That standoff matters for the dollar because credibility of the US policy framework supports the currency’s safe asset premium. Her departure would give President Trump an opportunity to secure a four-person majority on the seven-member board after another Biden appointee, Adriana Kugler, announced she would vacate her position early1.

Price action delivered an early read. Long dated Treasuries sold off as investors marked up a policy risk premium, while the broad dollar dipped only modestly before stabilising. We can infer that the market sees less near-term tightening impulse from a more politically directed Fed but also senses greater uncertainty around medium term inflation control. In other words, a steeper term premium with only a shallow initial hit to the dollar.

Strategic context and reserve currency reality

Beyond the cycle, the International Monetary Fund’s (IMF) latest update shows the dollar remains the dominant reserve asset, with a slow drift lower in share over the past two decades and a rise in smaller nontraditional currencies. That marks gradual erosion rather than outright replacement. Payment data tell the same story. The yuan is still roughly the sixth most used currency in global payments with a share below three percent, even as its infrastructure gains traction2. These facts are essential context for any claims that the dollar is being displaced.

BRICS and the limits of de-dollarisation

Brazil, Russia, India, China and South Africa (BRICS) matter within that context. Higher tariffs have accelerated the use of local currencies in Russia’s trade, and China-Russia commerce has reached record levels with a rising yuan share in settlements. That is meaningful for commodity flows and for the micro plumbing of regional trade finance. But it is still a long way from broad global payments shift. Liquidity, convertibility, rule of law, and deep collateral markets are the hurdles. Until BRICS can supply a scalable pool of safe assets with open capital accounts, local currency use will expand at the edges without dislodging the core.

Portfolio positioning with WisdomTree

For the remainder of the year, the balance of forces leans toward a softer dollar owing to the cooling of the US economy, weaker capital flows and a looser monetary cycle. Amidst the recent US dollar weakness, it is crucial for investors to maintain a balanced and diversified portfolio across asset classes. Four ways to diversify with WisdomTree product suite:

1)WisdomTree Hedged Physical Gold (GBSE and GBSP)

2)WisdomTree US Treasuries 30-year 3x Daily - short Treasuries (UL3S)

3)WisdomTree Short USD Long EUR currency (USEU)

4)WisdomTree Physical Bitcoin (BTCW)

Gold with currency hedging for euro and sterling investors

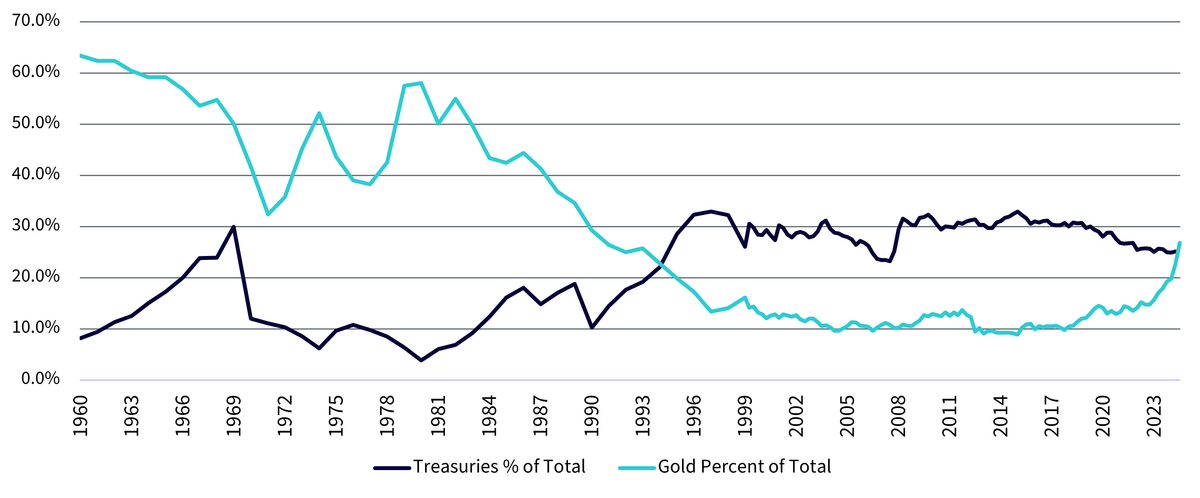

Foreign central banks now officially hold more gold than US Treasuries for the first time since 1996. That shift in reserve composition reinforces the case for gold as a portfolio diversifier.

Figure 2: Foreign Central Bank Hold more Gold than Treasuries

Source: FRED, Bloomberg, WisdomTree as of 30 June 2025. Historical performance is not an indication of future performance and any investments may go down in value.

One idea for euro and sterling-based investors is to enhance returns by using currency hedged gold exposure. Currency hedging allows investors to benefit more directly from movements in the gold price without the drag from adverse currency shifts. The WisdomTree Physical Gold – EUR daily Hedged (Ticker: GBSE) and WisdomTree Physical Gold – GBP daily Hedged (Ticker: GBSP) enables investors to gain efficient exposure to gold without managing physical holdings and foreign exchange instruments separately. These products are backed by London Bullion Market Association (LBMA) bars, ensuring deep liquidity.

Expressing political risk through the long end

If investors begin doubting the Fed’s autonomy, risk premiums on US assets could rise, borrowing costs may climb, and the dollar’s safe-haven status could be doubted. The WisdomTree US Treasuries 30-year 3x Daily - short Treasuries (Ticker: UL3S) stands out as the most direct trade: higher political risk means higher yields, lower prices, and amplified returns for inverse exposure. The WisdomTree US Treasuries 30Y three times daily short is a fully collateralised, UCITS eligible ETP that delivers a total return equal to three times the inverse daily performance of the BNP Paribas US Treasury Ultra Bond 30Y Rolling Future Index, which tracks front month Ultra US Treasury Bond futures, plus the interest earned on the collateralised amount. The US dollar may hold up briefly on yield support, but confidence in the dollar as the global benchmark could diminish, leading to longer-term downside.

Tactical currency tools

Currency ETPs (Exchange-Traded Products) can serve as tactical tools. These instruments replicate the relative movement of currency pairs and are widely used for hedging, speculation, or portfolio diversification. The WisdomTree Short USD Long EUR (Ticker: USEU) is an open-ended Collateralised Currency ETC designed to track the MSFX Short US Dollar/Euro Index (TR) which provides exposure to movements in exchange rates equivalent to a short position in USD forwards against EUR. These instruments are structured ETNs and are best used tactically rather than as long term core positions.

Bitcoin in the shadow of dollar fragility

Amid questions over Fed independence and the durability of the dollar’s safe-haven premium, bitcoin continues to emerge as an alternative monetary asset. Unlike fiat currencies tethered to political cycles and central bank discretion, bitcoin’s value proposition rests on algorithmic scarcity and decentralised governance. In periods when institutional trust is questioned - as with attempts to politicise Fed policy - bitcoin can benefit from a “credibility arbitrage”: capital rotating into an asset whose rules are seen as unalterable. While its volatility keeps it from being a wholesale dollar substitute, Bitcoin increasingly operates as a hedge against both monetary dilution and institutional risk. The narrative of “digital gold” becomes more powerful when the credibility of traditional anchors looks shakier.

Conclusion

Markets will spend the coming months balancing a softer policy path with a live test of institutional resilience. If the courts reaffirm protections for the Fed and Chair Powell steers a measured easing cycle, the dollar weakness is likely to be measured. If political pressure weakens that anchor, the risk premium embedded in rates and the currency will rise and the longer-term appeal of US assets will erode. For investors the practical response is to stay diversified, use hedges judiciously and watch three signposts: the legal trajectory of the Cook case, the tone of September policy communication and the progress of BRICS settlement rails. The destination is a world where the dollar remains first among many, but one that pays a premium whenever trust in its institutions is questioned.

1 Bloomberg as of August 1, 2025

2 SWIFT RMB Tracker, as of 31 July 2025

About the contributor

Director, Macroeconomic Research, WisdomTree Europe

@AneekaGuptaWTAneeka Gupta is Director of Research at WisdomTree. Prior to the acquisition of ETF Securities in April 2018, Aneeka worked as an Equity & Commodities Strategist at the company. Aneeka has 17 years of experience working as a Research Analyst across a wide range of asset classes. In her current role she is responsible for conducting analysis for all in-house equity, commodity and macro publications and assisting the sales team with client queries around products and markets. Prior to WisdomTree, Aneeka began her career as an equity analyst at Bear Stearns International Ltd in London. She also worked as an Equity Sales Trader at Sunrise Brokers across US and Pan European Exchanges. Before that she worked as an Equity Derivatives Sales Manager at Mashreq Bank in Dubai. Aneeka holds a Masters in Mathematics from Oxford University and a BSc in Mathematics from the University of Delhi, India. She is also a CFA Charterholder.