Enhancing gold exposure for non-USD investors

Published 11 June 2025

Key Takeaways

After a prolonged appreciation comes a depreciation phase for the US dollar

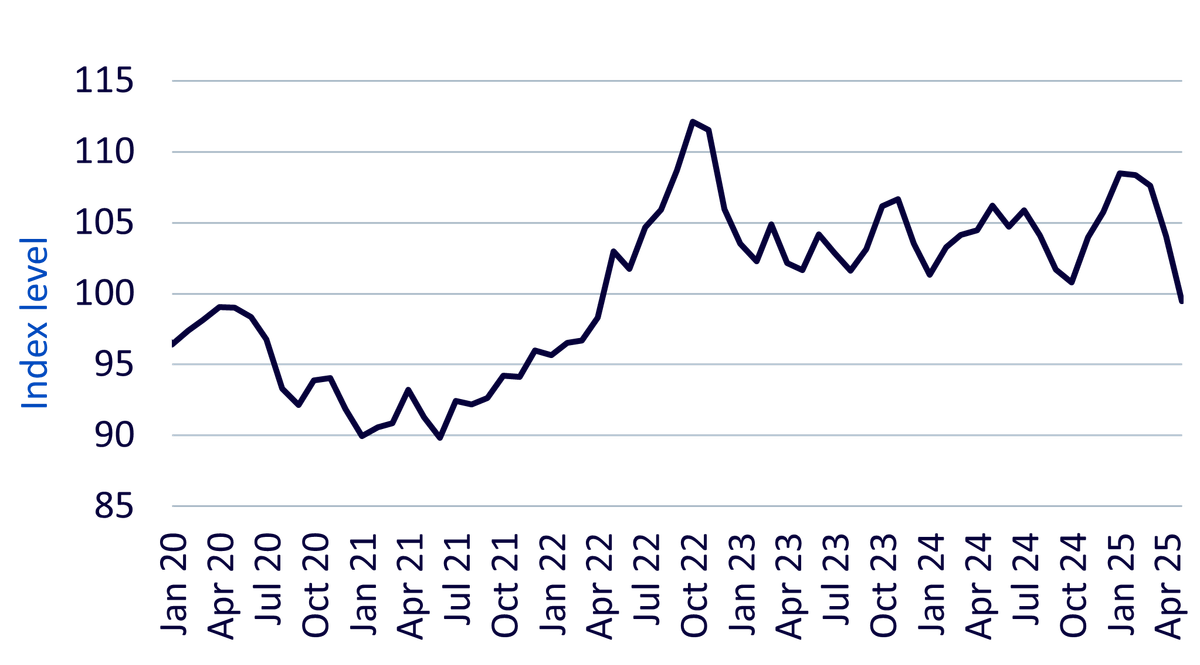

The US dollar basket appreciated significantly between May 2021 and September 2022, rising by 25% as the Federal Reserve (Fed) led the global monetary tightening cycle. However, from September 2022 to October 2024, the dollar mostly depreciated within a range, falling around 10%. A sharp rebound followed, with the dollar gaining 10% between October 2024 and January 2025. This surge was driven by the perception that the US economy was on a stronger footing than its peers, reducing expectations of imminent monetary easing by the Fed—supporting dollar strength.

The appreciation accelerated following Donald Trump’s victory in the November 2024 US presidential election. Markets anticipated pro-growth, low-tax policies would further boost the economy. However, since January 2025, the dollar has weakened considerably, with the dollar basket now trading well below its October 2024 trough. Much of the earlier optimism surrounding Trump’s policies has eroded, particularly amid rising concerns about demand destruction stemming from an escalating trade war. The dollar basket is now down nearly 10% from its January 2025 peak.

Figure 1: US dollar basket (DXY)

Source: WisdomTree, Bloomberg. January 2020 – April 2025. Monthly data. Dollar Basket (DXY) is a measure of the value of the US dollar against a basket of currencies (Euro, Swiss franc, Japanese Yen, Canadian Dollar, British Pound and Swedish krona). Historical performance is not an indication of future performance and any investments may go down in value.

Market outlook: further dollar weakness expected

Market sentiment suggests further dollar weakness. According to Bloomberg’s survey of foreign exchange analysts, the dollar basket is expected to decline from its current level of 100 to 97.6 by Q1 2026. Forward markets also indicate euro appreciation against the dollar, with the EUR/USD exchange rate projected to rise from 1.13 to 1.16 over the same period.

US dollar and gold

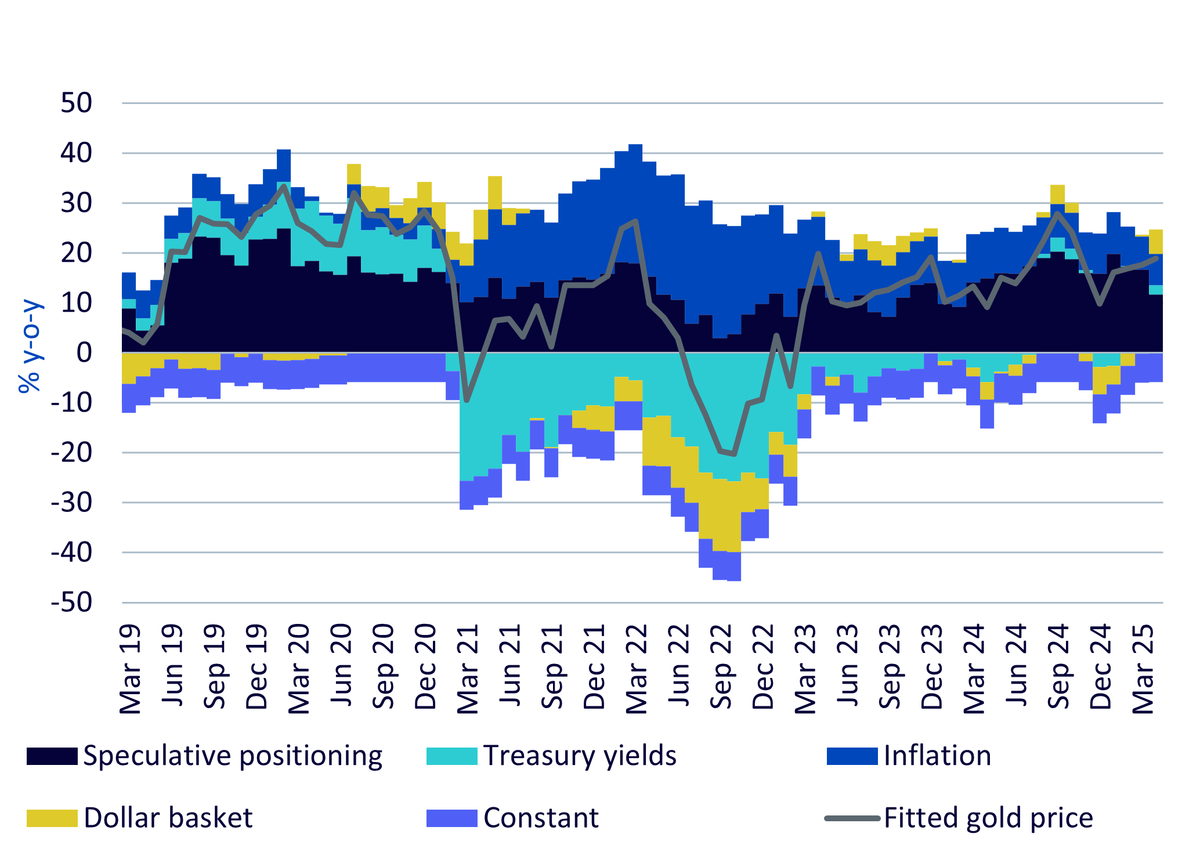

The US dollar exchange rate is a key driver of gold price behaviour in dollar terms. Our proprietary gold model shows that the dollar’s appreciation during 2021–2022 significantly weighed on gold performance. In contrast, dollar depreciation in 2023 contributed positively to gold prices. More recently, in March and April 2025, renewed dollar weakness once again supported gold gains.

Figure 2: Gold price attribution

Source: Bloomberg, WisdomTree price model, data as of April 2025. Fitted gold price is growth in gold price (year-on-year) expected by the model. The bars represent the components of the model. Speculative positioning is net non-commercial positioning in gold futures markets (that is, netting shorts away from long positions as reported by the Commodity Futures Trading Commission). Treasury yields is the nominal yield to maturity on a 10-year US Treasury Bond. Inflation is the annual growth of the US Consumer Price Index. Historical performance is not an indication of future performance and any investments may go down in value.

Capturing all gold gains for a non-USD investor

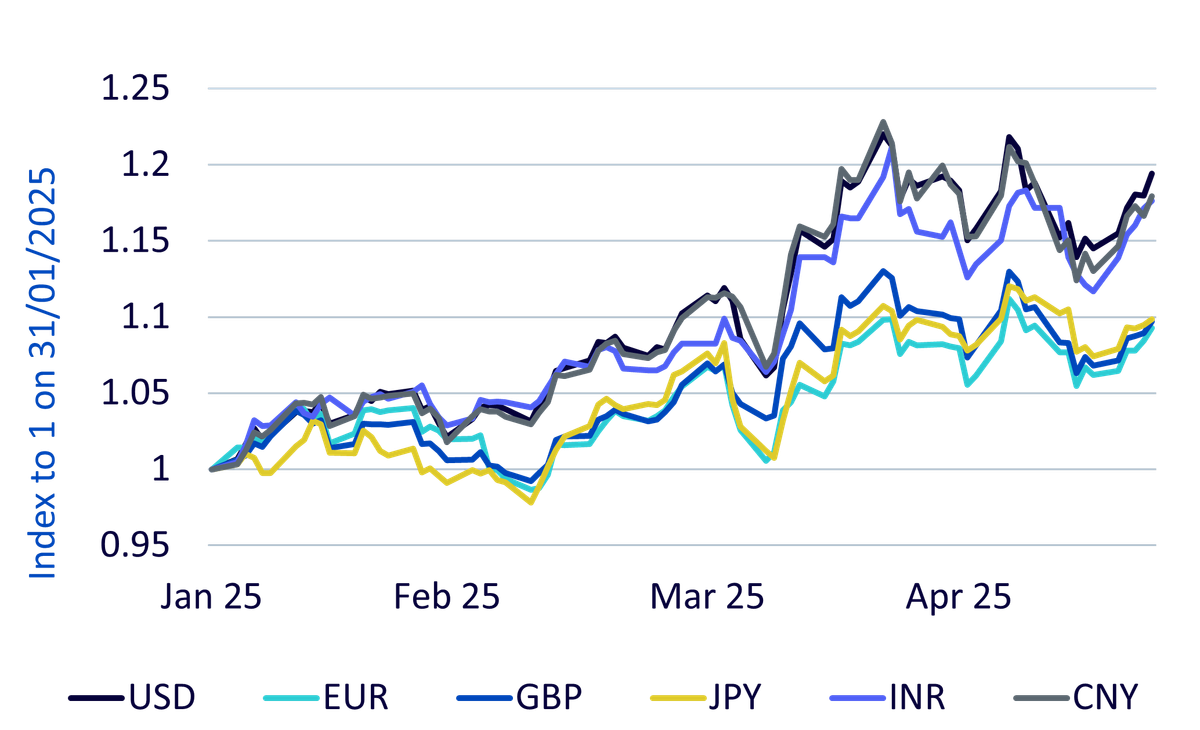

For investors managing portfolios in non-USD currencies, gains from gold’s appreciation due to dollar depreciation can be elusive—especially if the dollar is weakening against their home currency. As illustrated in the chart below, gold’s strongest performance has been in USD terms. In contrast, gold priced in EUR and GBP has appreciated only about half as much.

Figure 3: Gold performance in various currencies

Source: WisdomTree, Bloomberg. 1 January 2025 – 23 May 2025. Daily data. Historical performance is not an indication of future performance and any investments may go down in value.

Investors managing portfolios in EUR or GBP can enhance returns by using currency-hedged gold products. Currency hedging allows them to benefit more directly from gold price movements, without the drag from adverse currency shifts.

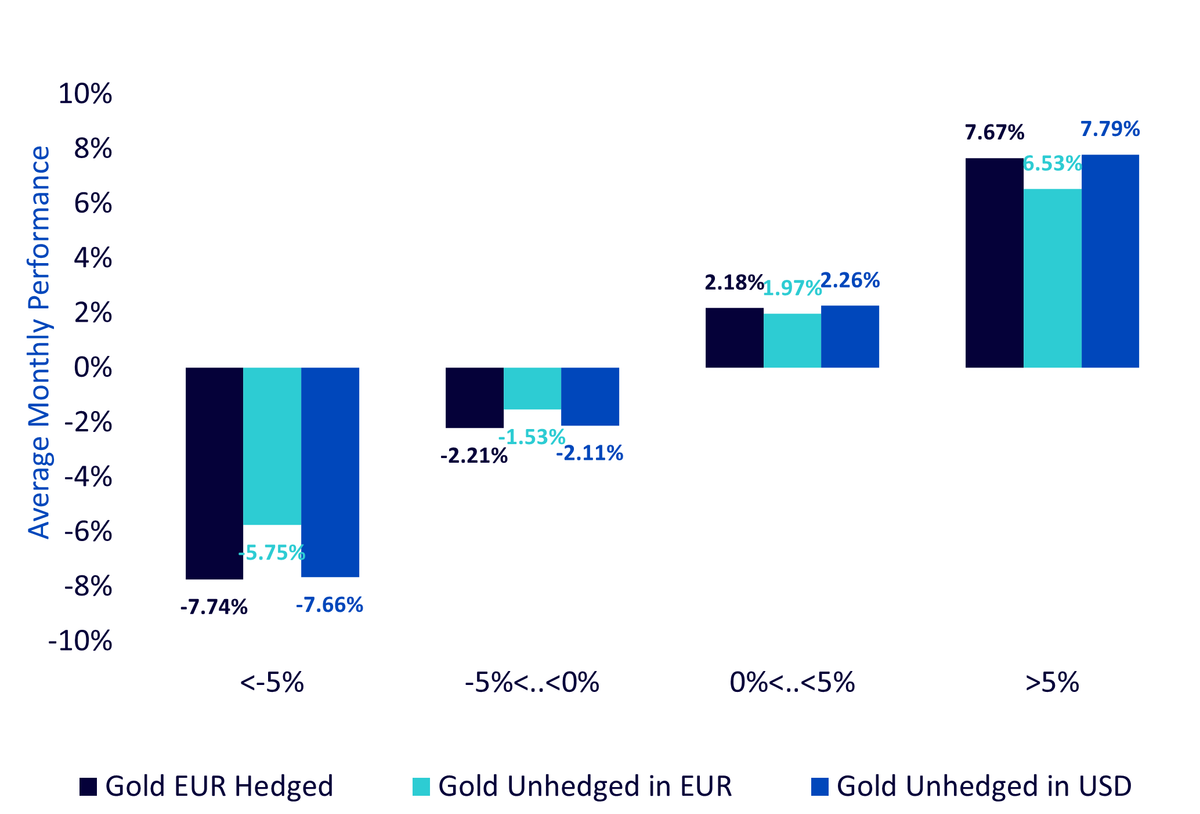

Historically, currency hedging has helped investors capture more of gold’s upside:

In EUR terms, since 2004, during months when gold prices rose more than 5%:

- Unhedged EUR gold exposure increased by 6.53% on average.

- USD gold increased by 7.79%, creating a gap of 1.26%.

- Currency-hedged EUR gold exposure rose 7.67%, narrowing the gap to just 0.12%.

Figure 4: Historic performance of gold, hedged and unhedged, EUR

Source: WisdomTree, Bloomberg. December 2003 – April 2025. Monthly data. Historical performance is not an indication of future performance and any investments may go down in value.

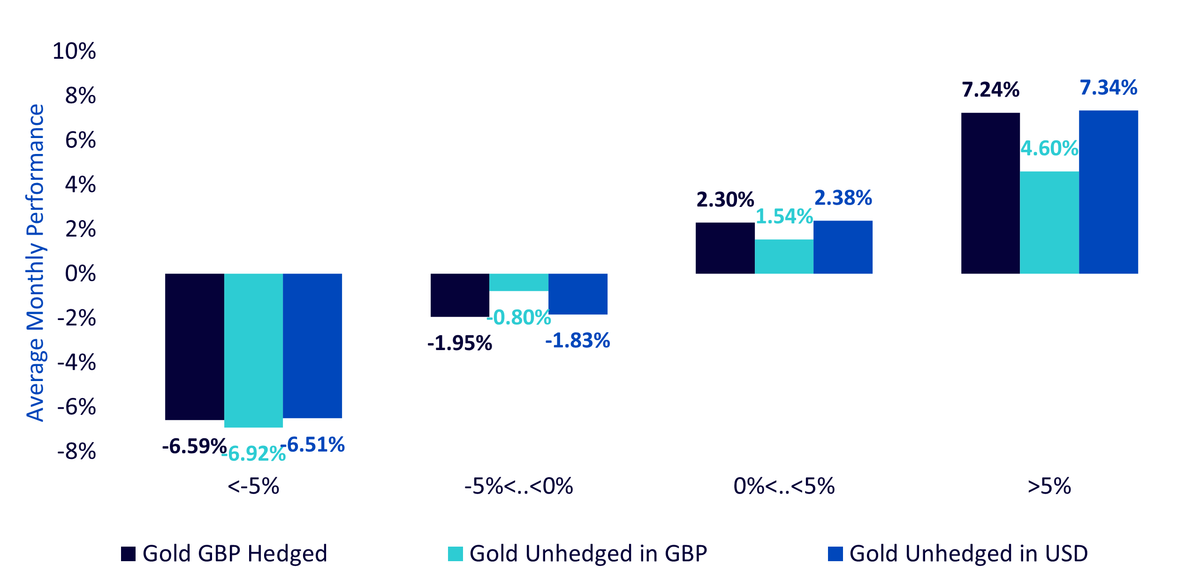

In GBP terms, since 2016, during similar gold surges:

- Unhedged GBP gold exposure increased by 4.60% on average.

- USD gold rose by 7.34%, a gap of 2.74%.

- Currency-hedged GBP gold exposure gained 7.24%, reducing the gap to just 0.10%.

Figure 5: Historic performance of gold, hedged and unhedged, GBP

Source: WisdomTree, Bloomberg. December 2016 – April 2025. Monthly data. Historical performance is not an indication of future performance and any investments may go down in value.

Categories

About the contributor

Head of Commodities and Macroeconomic Research, WisdomTree Europe

@NiteshShahWTNitesh Shah is a seasoned financial professional with over 24 years of experience in research and investment strategy. As Head of Commodities & Macroeconomic Research at WisdomTree Europe, he leads market analysis and insights across asset classes, with a focus on commodities and exchange-traded products. Previously, he held roles at Moody’s, HSBC Investment Bank, The Pension Protection Fund, and Decision Economics, building expertise in market analysis and strategy. Nitesh earned a master’s degree in International Economics and Finance from Brandeis University and a bachelor's in Economics from the London School of Economics. His insights are frequently featured in financial media, and he is a sought-after speaker at industry events. He also hosts the ‘Commodity Exchange’ podcast, where he discusses trends shaping global markets. Passionate about guiding investors, Nitesh provides actionable insights to help them navigate complex financial landscapes.