CORN LN

WisdomTree Corn

Published 26 September 2025

The September World Agricultural Supply and Demand Estimate (WASDE) presents investors with a very large US crop, raised export ambitions, and still‑ample ending stocks. Yet corn prices have stabilized back above $4 per bushel. The balance of risks over the next 3–6 months appear skewed modestly to the upside, with a path toward $4.50–$5.00 per bushel if yields slip a bit further and exports stay on their current pace, downside below $4 requires both a smooth US harvest and an aggressive Brazil/Black Sea export push.

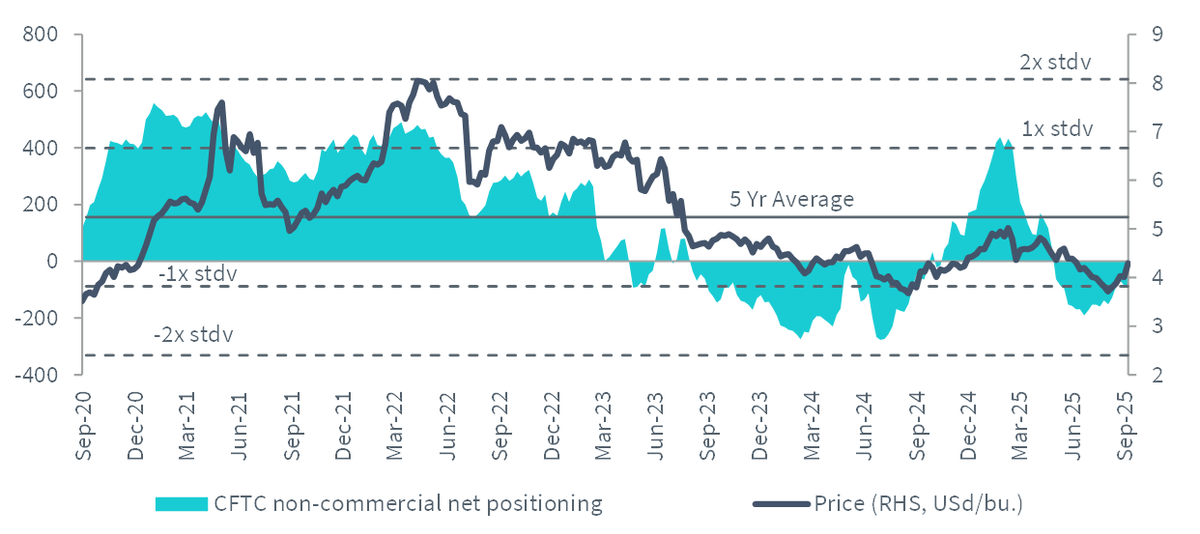

Sentiment on the corn market has shown signs of improvement last month. While still below the 5-year average, net speculative positioning in corn rose 43.6% helped by a 9% build up in long positions alongside a 9% trimming of short positions, last month.

Source: Bloomberg, Commodity Futures Trading Commission from 9 September 2020 to 9 September 2025. Historical performance is not an indication of future performance and any investments may go down in value.

Déjà vu at $4—but with stronger exports

The 2025/26 marketing year opens with a familiar backdrop with corn anchored near US$4/bushel, volatility driven by shifting yield estimates and a renewed debate over US export capacity. In September, the USDA trimmed yield versus August by 2.1 bushels per acre (bpa) to 186.7bpa but raised harvested area to 90mn acres (the largest since 1933), lifting production to 16.8bn bushels1. Exports were lifted by 100mn bushels to a record 3bn bushels on US export competitiveness and robust early‑season demand, leaving ending stocks at 2.1bn bushels, down by 7mn bushels. Those headline changes explain corn’s rebound after the August sell‑off with less yield, more demand, and only a marginal change in carryout.

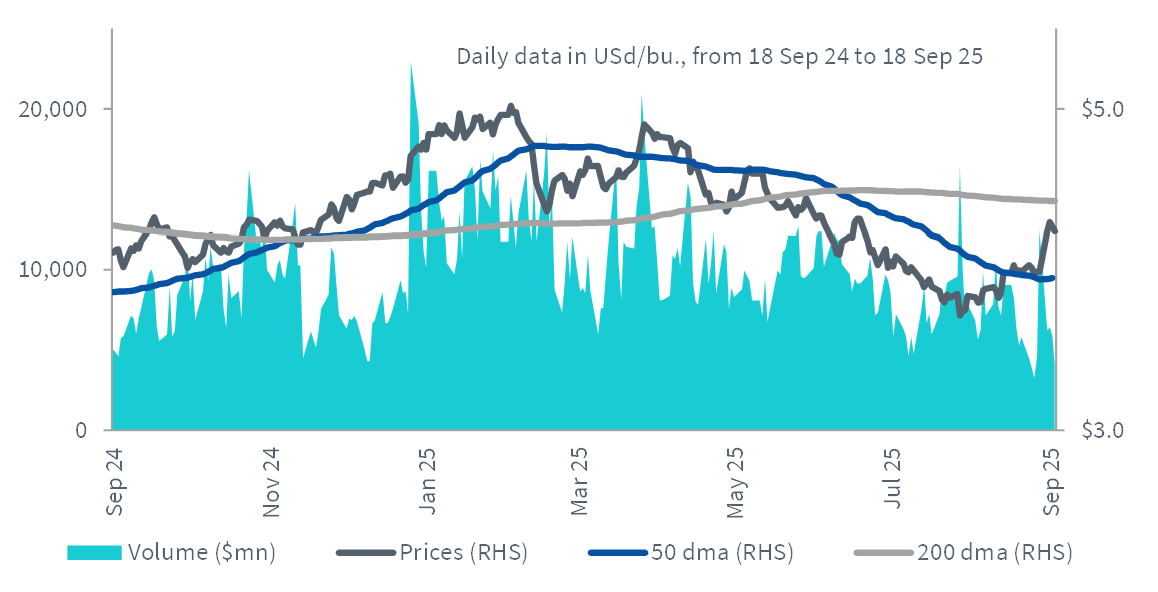

Source: Bloomberg, WisdomTree from 18 September 2024 to 18 September 2025. Historical performance is not an indication of future performance, and any investments may go down in value.

At the same time, the global picture is constructive at the margin. USDA expects lower European Union (EU), Serbian and Russian corn production to offset higher production in Canada, India and the United States . Additionally global trade is up as the US and Zambia are forecasted to export more outweighing lower exports from Serbia, the EU and Russia. Global imports are also forecasted higher on the back of higher imports for the EU. World corn ending stocks were nudged down to 281.4mn Metric Tons (Mt) 2. A small change, but one that works with, not against, the firmer US tone.

Supply: the US balance still pivots on yield risk

US corn is still a yield-driven market. The USDA’s 186.7bpa projection is still a record figure that implies ample supplies, but prices will hinge on whether forthcoming updates push that estimate higher or lower relative to August. Field reports this summer highlighted heat spikes in July and a dry turn across parts of the eastern Corn Belt in August. USDA captured the net effect by trimming yield while acknowledging the much larger harvested area. If subsequent crop production surveys verify more disease pressure or tip moisture variability a bit more negative, there is room for another modest reduction to yield.

Outside the US, the supply tone is mixed. Brazil remains formidable: USDA holds 2025/26 output at 131Mt (after 135 Mt in 2024/25) , ensuring the South American export machine stays very relevant through the Northern Hemisphere winter export window. Ukraine is pegged at 32Mt, restoring some Black Sea presence. But EU production is lower, and EU imports are raised, shifting part of global demand back onto seaborne exporters, including the US, during Q4/Q13.

US Demand: feed, Ethanol and Exports look serviceable

USDA raised 2025/26 feed & residual to 6.10bn bushels, up year‑on‑year as cheaper corn, firm poultry output and steady pork availability nudge rations back toward corn. Industrial use is set at 6.98bn bushels, with 5.60bn bushels for ethanol—essentially a small annual gain that mirrors stable domestic gasoline demand plus a healthier export channel for ethanol. Inventories of ethanol ended last year lower, and crush margins improved into late summer, both consistent with USDA’s small increase.

The biggest swing factor and the biggest positive revision in September was exports. USDA’s 3bn bushels target is ambitious but credible. The foreign balance sheet helps (EU shortfalls and higher import needs), and the US is price‑competitive into key destinations when Gulf basis is seasonally soft at harvest. USDA is explicit that the revision reflects robust early‑season demand.

Conclusion

The September WASDE subtly tightened the balance by pairing a smaller yield with a higher export number, while leaving carryout only marginally changed. Beneath the surface, global adjustments (lower EU crop, higher EU imports, a slight dip in world stocks) offer just enough help to US corn in the winter export window. From here, modest yield downticks and sustained early‑season export strength are all it would take to provide a tailwind for corn. Conversely, flawless US harvest execution alongside heavy Brazil/ Black Sea competition would cap rallies.

Director, Macroeconomic Research, WisdomTree Europe

@AneekaGuptaWTAneeka Gupta is Director of Research at WisdomTree. Prior to the acquisition of ETF Securities in April 2018, Aneeka worked as an Equity & Commodities Strategist at the company. Aneeka has 17 years of experience working as a Research Analyst across a wide range of asset classes. In her current role she is responsible for conducting analysis for all in-house equity, commodity and macro publications and assisting the sales team with client queries around products and markets. Prior to WisdomTree, Aneeka began her career as an equity analyst at Bear Stearns International Ltd in London. She also worked as an Equity Sales Trader at Sunrise Brokers across US and Pan European Exchanges. Before that she worked as an Equity Derivatives Sales Manager at Mashreq Bank in Dubai. Aneeka holds a Masters in Mathematics from Oxford University and a BSc in Mathematics from the University of Delhi, India. She is also a CFA Charterholder.