BTCW LN

WisdomTree Physical Bitcoin

Published 23 March 2026

Director, Digital Assets Research

The debate has shifted. The question is no longer ‘should we allocate to crypto?’ but ‘how do we implement it properly?’.

Institutional crypto adoption has crossed an important threshold. Investment committees are no longer debating legitimacy. They are debating sizing, structure and governance.

A 2% allocation may appear modest in capital terms, but it is not modest in impact. Properly constructed, that exposure can materially improve portfolio convexity while keeping volatility contribution contained. The institutional challenge is no longer access. It is architecture.

Bitcoin remains the institutional anchor. It benefits from:

From a portfolio standpoint, bitcoin expresses the digital hard money thesis: scarcity, monetary neutrality, and macro sensitivity to real yields and global liquidity conditions.

| 60/40 Global Portfolio | 1% Bitcoin Portfolio | 3% Bitcoin Portfolio | 5% Bitcoin Portfolio | 10% Bitcoin Portfolio | MSCI AC World | Bloomberg Multiverse | Bitcoin |

|---|---|---|---|---|---|---|---|---|

Annualised Return | 6.40% | 7.01% | 8.23% | 9.44% | 12.43% | 9.83% | 1.01% | 48.75% |

Volatility | 8.76% | 8.83% | 9.12% | 9.57% | 11.30% | 13.90% | 4.99% | 65.30% |

Sharpe Ratio | 0.52 | 0.59 | 0.70 | 0.80 | 0.94 | 0.58 | -0.16 | 0.72 |

Information Ratio | 0.93 | 0.93 | 0.92 | 0.92 | ||||

Sortino Ratio | 0.63 | 0.71 | 0.86 | 0.98 | 1.20 | 0.68 | -0.22 | 0.97 |

Beta | 69% | 71% | 73% | 75% | 80% | 100% | 24% | 178% |

Source: Bloomberg, WisdomTree. From 31 December 2013 to 31 December 2025. In USD. Based on daily returns. The 60/40 Global Portfolio is composed of 60% MSCI AC World and 40% Bloomberg Multiverse. You cannot invest directly in an index. Historical performance is not an indication of future performance and any investment may go down in value.

For investors prioritising governance simplicity, a bitcoin-only allocation is operationally efficient and strategically coherent. However, bitcoin captures only one structural driver: monetary scarcity. It does not capture:

The institutional decision is therefore not binary. It is thesis-driven.

Is the allocation purely monetary? Or is it a broader bet on digital financial infrastructure?

Crypto in 2026 is increasingly adoption-led rather than purely price-led. The ecosystem now reflects economically distinct drivers:

Institutions must decide which adoption vectors they wish to underwrite.

Historically, crypto exposure was synonymous with price volatility. It was treated as high-beta convexity. That framing is increasingly incomplete.

Proof-of-stake networks such as Ethereum and Solana convert protocol security into economic yield. Validators secure networks and are compensated for participation. This transforms certain digital assets into income-generating instruments.

Staking introduces three structural changes to portfolio construction:

This is critical. Crypto is evolving from a pure beta allocation into a total return sleeve.

Staking yield also reframes crypto from speculative exposure to productive digital capital.

The 2% allocation threshold is not arbitrary. It reflects risk-budget pragmatism.

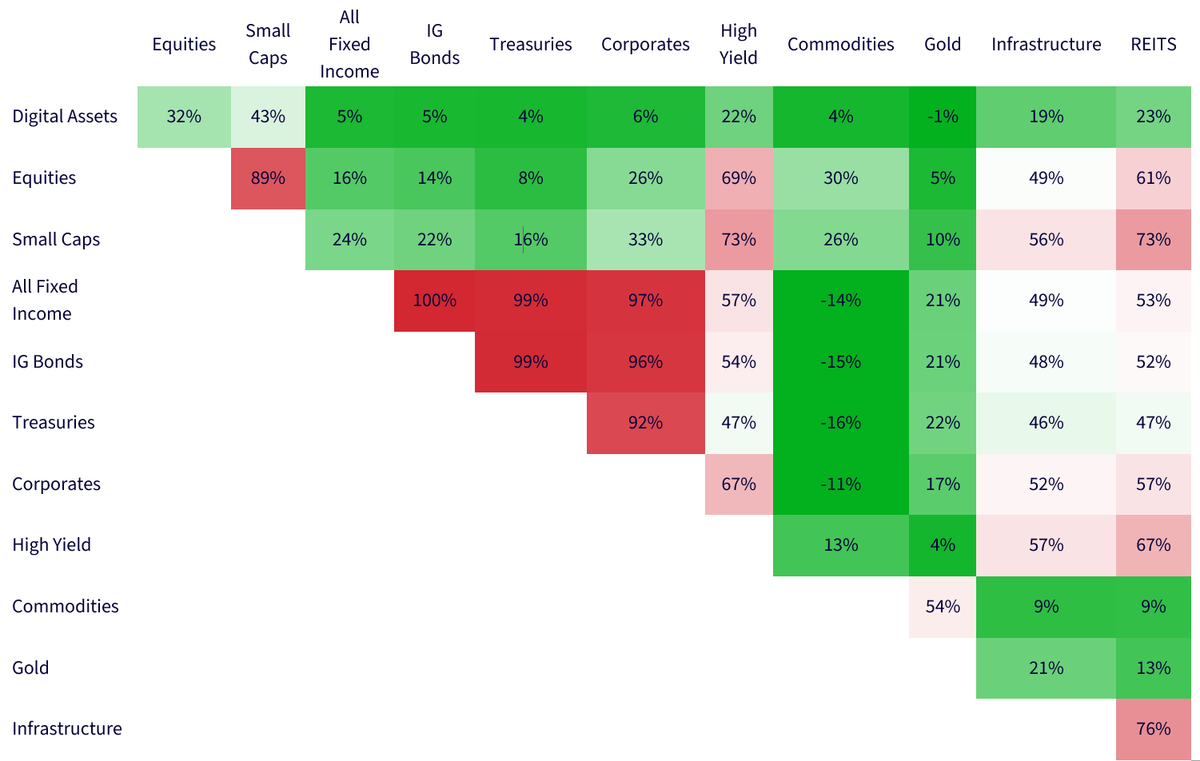

Bitcoin and broader crypto assets have historically exhibited low structural correlation to traditional equities and bonds across multi-year windows. While short-term correlations spike during liquidity shocks, long-term correlation regimes remain differentiated.

Source: Bloomberg, WisdomTree. From 31 January 2024 to 31 January 2026. In USD. Based on weekly returns. You cannot invest directly in an index. Historical performance is not an indication of future performance, and any investment may go down in value.

At small weights, return contribution becomes visible at a portfolio level, while volatility contribution remains modest. Maximum portfolio drawdown impact also remains contained.

However, this only holds under disciplined governance. It is of the utmost importance to stick to pre-determined rebalancing frequency (for example, quarterly or semi-annual) and avoid any panic buying or panic selling.

Without discipline, crypto allocation behaves like speculation. With discipline, it behaves like a diversifying growth sleeve.

If investors want structural exposure to digital assets without turning portfolios into single-coin bets, the answer is straightforward: start with a crypto basket ETP, then add conviction.

Index | Exposure |

|---|---|

CoinDesk 20 | Broad crypto market |

CoinDesk 5 | Core crypto market |

CoinDesk 5 Equal Weight | Balancing the leaders |

CoinDesk 10 Capped ex Bitcoin | The growth frontier |

Source: WisdomTree. March 2026.

A structured allocation separates strategic beta from tactical views. For example, within a 2% total crypto allocation:

This mirrors established equity portfolio construction, where broad market exposure is complemented by deliberate active tilts. The difference is that in crypto, the dispersion between assets is significantly higher, so starting with diversified exposure is even more critical.

Crypto basket ETPs matter because of:

In a maturing asset class with increasing institutional participation and dispersion across networks, broad crypto basket ETPs provide the structural backbone. Satellites add conviction. The combination restores control without sacrificing upside.

Bitcoin remains the institutional default: liquid, defensible and macro-coherent.

But digital assets in 2026 are broader than monetary scarcity. They encompass infrastructure, computational demand and income generation.

A 2% allocation is small in capital terms but meaningful in structural exposure. When properly constructed, it can enhance portfolio efficiency and improve convex return potential while containing risk contribution.

The institutional risk is no longer whether to allocate. It is allocating without structure.

Director, Digital Assets Research

Dovile Silenskyte is a director of digital assets research at WisdomTree. Before joining WisdomTree in May 2024, Dovile worked as an index equity product strategist at BlackRock. Currently, she is responsible for conducting analyses for in-house digital assets publications and assisting the sales team with client queries about products and markets. Dovile holds an MSc in Finance from Texas A&M University – Commerce, and she is also a chartered financial analyst (CFA).